Liquidity Adjustment Facility (LAF) – Full Form, Meaning, and Detailed Explanation

Full Form of LAF: Liquidity Adjustment Facility

LAF Liquidity Adjustment Facility (LAF) is a monetary policy tool used by Reserve Bank of India (RBI) to aid banks in case of any liquidity crisis or when they fail to meet the fund requirements. The LAF runs a cushion for commercial banks and financial institutions as it acts to open a window to borrow from the RBI on condition of falling short of funds, or parking unwanted surplus funds lying with the RBI without any return. This way, it assists in efficient cash flow management, financial stability and effective implementation of the monetary policy.

The LAF commands widespread attention in an economy like India’s, where liquidity requirements vary daily as a result of loan disbursals, seasonal demand, government operations and other day-to-day needs.

What Does LAF Mean in the Context of Banking?

LAF is something that people use in the banking world. The term LAF stands for Liquidity Adjustment Facility, which’s a thing that banks use to manage money. In terms LAF is a way for banks to borrow or lend money to each other or, to the central bank to make sure they have enough cash to do their daily business.

This helps the banks to keep a balance of money so they can give loans to people and businesses and also meet their own needs. So LAF is a part of how banks work and it helps to keep the banking system running smoothly. The bank has something called the Liquidity Adjustment Facility or LAF for short which’s a tool to deal with short term liquidity risks in a simple and efficient way.

Banks have to handle a lot of money every day. This can be a real challenge. The amount of cash that banks have can go up and, down a lot. If they do not manage this properly it can cause big problems with the way the bank operates. This can then affect the banks ability to lend money settle transactions and keep the system stable. The Liquidity Adjustment Facility is a way to make things more stable. It does this in two ways:

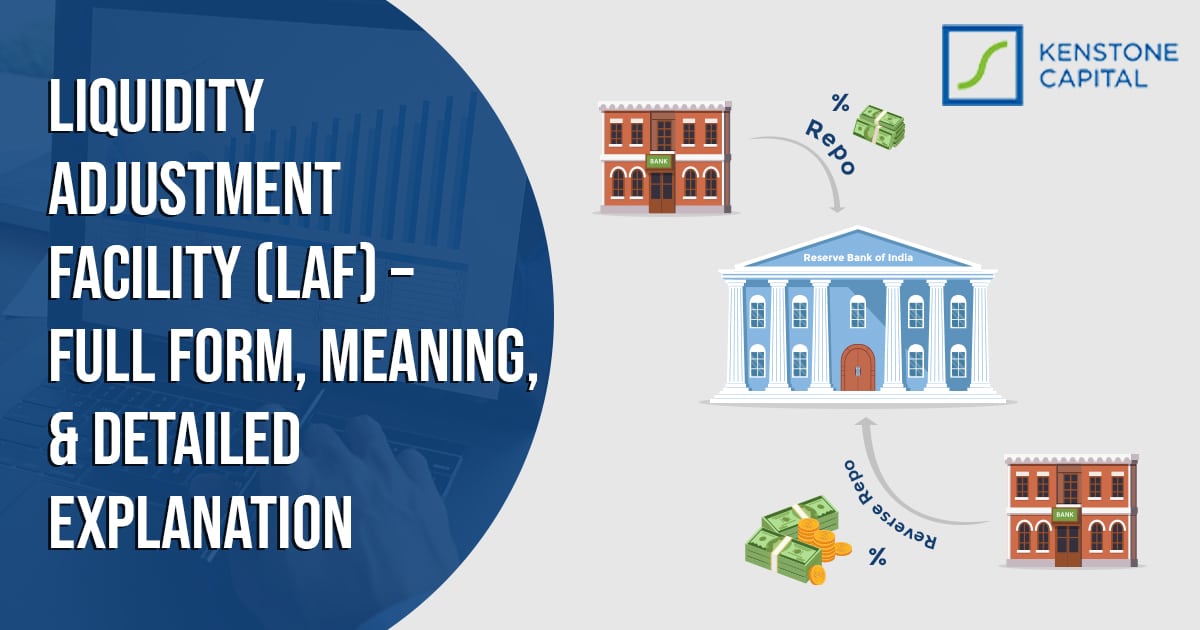

1. Repo Operations:

The Reserve Bank of India has a system where banks can borrow money from the Reserve Bank of India using government securities that the Reserve Bank of India approves of. These borrowings are usually for a period of time. The Reserve Bank of India loans money to banks for a short time like just one night or for a maximum of 14 days. This helps banks when they do not have cash.

The Reserve Bank of India helps banks a lot when people need cash like at the end of the quarter or during festivals. The Reserve Bank of India also helps banks when they are having problems. The Reserve Bank of India is very important for banks, during these times. Banks borrow money from the Reserve Bank of India to cover their cash shortages.

2. Reverse Repo:

Banks have some money they can put that money with the Central Bank, which is the Reserve Bank of India and they will get some interest on it. This interest is called the reverse repo rate. So when banks do this some money is taken out of the system. This helps to balance the amount of money that’s available. The Central Bank uses reverse repo to control the money supply.

Reverse repo is an useful tool for the Central Bank. It helps to prevent much money from being, in the system, which can cause prices to go up and that is called inflation. The Reserve Bank of India uses reverse repo to make sure that the money supply is just right and the Reserve Bank of India does this to prevent inflation.

LAF enables banks to be operationally efficient, mitigate the risk of short, term funding, and help maintain the order in the financial system through such mechanisms as described above.

How Liquidity Adjustment Facility Works

LAF operations revolve around a straightforward yet very efficient system for handling short, term liquidity:

Collateral-Based Borrowing through Repo Operations

In the case of a momentary shortage of liquidity a bank is allowed to take a loan from the RBI by providing securities of the government that are eligible for the purpose of collateral. This procedure called a repo agreement usually covers a period of a few days starting from overnight up to 14 days.

Through the repo, a bank can take a short, term cash bridge without having to liquidate its long, term investments. The interest is charged at the repo rate, which is determined by the RBI and is influenced by market conditions and the monetary policy. Through repo operations banks get a chance to continue lending and have smooth operations even in the case of financial stress or during seasonal spikes in cash demand.

Parking Surplus Funds through Reverse Repo

Bank holding extra cash in the form of surplus liquidity can place the extra funds with the RBI under a reverse repo agreement and at the same time gain interest at the prevailing reverse repo rate. By means of this instrument, banks are permitted to carry out their idle funds profitably while at the same time the excess liquidity is absorbed from the system thus preventing oversupply of money that leads to inflation.

Reverse repo operations are the instruments that provide banks with the opportunity to maintain a balanced liquidity position and at the same time get some returns in a safe manner while they are supporting the stability of the system.

Daily Auctions by the RBI

The Reserve Bank of India does something called LAF operations every day. They have auctions where banks can come and borrow money if they need it or put in money if they

money to spare. The Reserve Bank of India uses this auction system so everything is out in the open and fair. It helps them make sure money is being used in the way possible and they can keep a close eye on what is going on with money in the country.

By doing these operations the Reserve Bank of India can control the interest rates that banks use when they lend money to each other. This helps to keep the money market stable which is very important for the Reserve Bank of India and, for the country’s economy. The Reserve Bank of India uses the LAF operations to make sure everything runs smoothly.

System-Wide Impact of LAF

LAF transactions affect the entire banking system by directly influencing liquidity, short-term credit availability, and interest rates. By providing a structured framework for banks to manage daily cash flows, LAF ensures smooth lending, operational efficiency, and stability in interbank markets. Beyond supporting day-to-day banking, LAF serves as a strategic tool for the RBI to implement monetary policy, stabilize short-term interest rates, and foster confidence in India’s financial system.

Key Features of LAF

The Liquidity Adjustment Facility (LAF) is a boon not only to banks but also to the economy at large. It consists of certain essential features that enable it to function effectively. These features cooperate to ensure that banks have money to lend, interest rates do not fluctuate wildly, and people can still get money when they need it. Let’s examine each component of the Liquidity Adjustment Facility in detail.

Short-Term Liquidity Management

LAF mainly serves the short term liquidity requirements of banks, the duration being generally overnight, 7, day, or 14, day. Banks daily cash flow is affected in different ways and that is why they experience daily fluctuations in cash flow. The factors responsible for these fluctuations are customer withdrawals, loan disbursements, inter, bank settlements, and government transactions.

The Liquidity Adjustment Facility or LAF is very significant for banks. In the absence of the Liquidity Adjustment Facility, banks could find themselves in a difficult situation when they are short of money for a brief period of time.

This can lead to problems in the way the banking system operates and make it difficult for people to get loans. The Liquidity Adjustment Facility supports banks by allowing them to borrow money for a period or to deposit the surplus money. In this way, banks can continue to work and deal with times when there is temporary cash shortages, and meet regulatory requirements such as the cash reserve ratio (CRR). This short-term focus provides a critical buffer for operational stability.

Dynamic Interest Rates

The repo and reverse repo rates under LAF are dynamic. They change based on RBI monetary policy and current market conditions. This system promotes disciplined liquidity management. It works in a similar regulatory environment where banks must follow RBI guidelines for debt collection to ensure transparency and compliance.

When the repo rate is high, banks do not borrow and put excess funds in reverse repo at a better Return. Lower the repo rate, lower the cost of borrowing. Banks subsequently procure funds from the RBI for liquidity over the short term. The structure maintains equilibrium in the market.

It influences banks’ criteria for borrowing and lending. The result corresponds to general economic aims such as inflation management, credit expansion, financial restraint and economic stimulation.

Execution Effectiveness

By providing daily modification of banks’ liquidity positions, LAF is critical to the sound functioning of the banking system. Routine adaptability allows banks to : Prevent cash deficiencies that might interfere with credit, settlement or customer dealings. Ensure that idling funds are actively employed to avoid any deterioration in financial return.

Through exact daily control of the liquidity, LAF supports continuous banking operations smooth interbank dealings and improved financial planning. Such efficiency of operations also mitigates the contingency of emergency borrowing at a costlier rate, aiding the banks to remain profitable and abide by regulatory prescriptions.

Equilibrium in Money Markets

LAF primarily ensures stability in the money markets. LAF shapes the interbank (call money and notice money) and short-term (up to 14 days) interest rates by deploying the instruments of repo and reverse repo so that the volatility in the market rates over the day is checked. Consistent rates:

• Increase assurance of banks and financial bodies.

• Guarantee consistency in immediate borrowings and lendings.

• Facilitate efficient pass-through of monetary policy to the economy.

Without LAF, abrupt liquidity demand or supply shocks might result in extreme volatile interest rates, disturbing banks, corporates and investors. LAF’s stabilization guarantees the credibility of the short-term money markets, facilitating seamless economic operations and system-wide strength.

Economic Influence of LAF

LAF is a major monetary policy tool besides being a liquidity management tool. Its activities immediately affect the circulation of credit, the rates of interest and the whole of economic activity.

1. Throughout Elevated Inflation Periods:

- Boosted repo rate by the RBI that inflate the cost of borrowing from banks.

- More expensive credit depresses credit to firms and households, checks inflation and steady prices in the economy.

2. During Economic Slowdown:

- The Reserve Bank of India lowers the repo rate, which means it is cheaper for banks to borrow money from the Reserve Bank of India. This is a help, for the banks because they can get the money they need at a lower cost. The Reserve Bank of India does this to help the banks and the people who need to borrow money. The Reserve Bank of India is trying to make it easier for people to get loans and for businesses to grow.

- This helps businesses to get loans and invest in things, which makes them grow and do more business and that is good, for the economy because it helps when things are slow.

In April 2019 some people who study the economy thought that the Reserve Bank of India or the RBI would lower the repo rate by 25 basis points. They did this because the RBI wanted to deal with inflation slow economic growth and weak global demand for things. When the economy started to get better the RBI was expected to raise the repo rates by 2020. The reason for this was to keep prices stable. The RBI had to make sure that the economy was growing at a good pace and that prices were not rising too fast. The RBI and the economy are very important so the RBI had to make decisions, about the repo rates to help the economy and the RBI.

Through such mechanisms, LAF not only provides operational support to banks but also becomes a strategic tool for the RBI to influence economic growth and inflation levels.

Why LAF is Important for Banks and the Economy – Detailed Explanation

The Liquidity Adjustment Facility is really important for banks in India. It does a lot more than just help banks with their work. The Liquidity Adjustment Facility is a part of keeping the financial system in India stable and running smoothly. It also helps the banks work well. Helps the government make economic policies that work. We can see how important the Liquidity Adjustment Facility is when we look at how banks do their day to day work and also when we look at the picture of the whole economy, in India.

1. Liquidity Cushion

Banks have to deal with changes in the money that comes in and goes out every day. This happens because of things, like people taking out cash banks giving out loans and the government doing transactions. Banks also have things they need to pay for.

The Liquidity Adjustment Facility is a way for banks to get the money they need for a time when they do not have enough. Banks can borrow this money. They can put extra money they have into the facility.

By doing this banks can keep everything running smoothly. They do not have to do things that might not be the choice just because they need money quickly. They also do not have to borrow money at rates that’re too high. Banks can use the Liquidity Adjustment Facility to borrow money through something called a repo agreement. They can put extra money into it through a reverse repo. This cushion is particularly critical during periods of financial stress, seasonal demand spikes, or sudden market disruptions, helping banks maintain uninterrupted credit availability and operational stability.

2. Monetary Policy Support

LAF is one of the main tools with which the RBI carries out its monetary policy. By changing the repo and reverse repo rates, the RBI can influence directly the cost and availability of credits in the banking system. As an illustration:

In times of high inflation, an increase in the LAF repo rate discourages excessive borrowing thus controlling the supply of money and the growth of prices. In a period of economic downturn, a reduction in the repo rate makes a short, term loan less expensive thus encouraging businesses to invest and therefore increasing economic activity. By these means, the LAF serves as a channel for the RBI to manage short, term liquidity, control interest rates, and indirectly influence inflation, investments, and consumption patterns in the economy.

3. Financial Discipline Encourages

The well-defined LAF framework helps banks to be responsible for the management of their liquidity situation and refrain from seeking LAF in an unplanned or emergency manner. Banks are encouraged to have enough liquid cash, to prepare for their daily cash flow, and to closely monitor their short, term funding needs. The mentioned financial discipline reduces the risk of sudden liquidity crises, guarantees compliance with regulatory requirements, and entails the banking sector’s stability. Basically, LAF is not only a device to offer temporary respite but it also contributes to banks’ long, term operational prudeness.

4. Supports Digital and Modern Banking

The shift towards digital transactions, fintech platforms, and the Digital Rupee have collectively made it essential for banks to maintain efficient liquidity. In order to execute digital payments, extend loans, and carry out banking, related technological innovations, banks need to be able to acquire short, term funds without any hurdles. Through the banker, liquidity window, the banks can continue to function effortlessly in a contemporary digitally, driven financial environment while abiding by the ever, changing regulatory frameworks such as the RBI rules for digital lending apps. Aside from this, it is an important measure towards increasing operational efficiency and consequently, customer trust and confidence in banking services.

Broader Implications of LAF

The Liquidity Adjustment Facility (LAF) plays a vital role in shaping India’s financial and economic stability. Its impact goes far beyond providing day-to-day liquidity to banks. Through its repo and reverse repo mechanisms, the RBI influences how money flows through the system, how interest rates behave, and how financial institutions take decisions about lending, borrowing, and investment. These effects can be felt across the wider economy, making LAF a central tool in the RBI’s monetary policy framework.

Stabilizing Interest Rates Across the Economy

Interest rate stability is one of the major consequences of LAF. By adding or removing liquidity as necessary, the RBI keeps short-term interest rates from showing sudden spikes or drops. Such stability is very important to banks because it gives them the opportunity to plan their lending activities with more certainty. Borrowers are also in a good position with predictable interest rates, making loans and credit products more manageable. Without LAF, the financial system would be more volatile, thus, borrowing would be riskier and more expensive for businesses and individuals.

Supporting Sustainable Credit Growth

Moreover, LAF is instrumental in achieving stable and sustainable credit growth. In times of banking sector liquidity shortages, banks can have recourse to the repo operations, thus, can continue issuing loans to consumers and businesses. The absence of such situations in economic activities such as business expansion, consumer purchases, and investment is ensured. When there is excess liquidity in the market, reverse repo operations enable banks to park funds with the RBI, thus, avoiding loans that are uncontrolled or speculative. Hence, LAF is a credit growth tool that works in harmony with broader macroeconomic objectives and keeps the money flowing in a responsible way.

Enabling Efficient Capital Allocation

Efficient capital allocation is a consequential benefit of the LAF framework. Banks are prompted to deploy funds more productively, thereby deciding between lending, investing in government securities, or depositing surplus liquidity with the RBI. This process removes the practice of keeping funds idle and ensures that financial resources are utilized in areas where they bring value to the economy. As liquidity conditions change, banks modify their strategies, thus bringing back the sector, wide discipline and accountability.

Boosting Confidence in the Banking System

LAF is a significant factor in trust and stability within the banking ecosystem. Banks become confident that they will be able to handle sudden liquidity pressures through the RBIs mechanisms. Hence, there is a reduction in panic, emergency asset sales, and unpredictable disruptions. A stable liquidity environment is a source of reassurance for investors, depositors, and borrowers, and thus, they receive an unambiguous signal that the RBI is actively supporting market balance. With enhanced confidence, the financial system is less vulnerable to shocks, whether domestic or global.

Why the LAF Framework Matters for the Economy

The Liquidity Adjustment Facility is not only a technical monetary tool. It affects interest rates, choices of lending, use of capital, financial discipline, and market sentiment. Its major effects, therefore, help economic stability, keep the banking sector safe, and make India’s financial system capable of responding to market fluctuations and uncertainties. As a result, LAF represents a core instrument in the RBI’s monetary policy plan and continuously contributes to the strengthening of India’s economic framework.

Conclusion

The Liquidity Adjustment Facility (LAF) is far from being only a short-term funding tool. It is a strategic instrument that supports the stability of India’s banking system, facilitates the RBI’s monetary policy goals, and makes it possible for banks to function efficiently in a changing financial environment. The knowledge of LAF is vital for banking professionals, financial analysts, policymakers, and any individuals interested in the financial ecosystem of India.