What is Accounts Receivable Factoring?

Accounts receivable factoring is a straightforward working capital financing trick that helps businesses get cash for their invoices immediately instead of waiting weeks for a customer to pay. This setup is great for liquidity management because it stops cash flow gaps before they start and helps with cash flow optimization without the headache of bank loans.

While it’s a lifesaver for growth, it does come with a cost. You’re essentially paying a debt recovery agency in India or a “factor,” to handle your ledger management through two specific fees: a management commission and a finance commission.

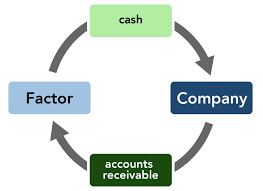

How Does Accounts Receivable Factoring Work?

The process for factoring receivables is pretty simple across the board. A lending partner, the factor, buys your unpaid invoices at a discount so you get cash right away. This accounts receivable factoring cycle ends when the factor collects the full payment from your client and sends you the remaining balance minus their fees.

Basically, factoring of accounts receivable hinges on how reliable your customers are. By leaning on AR factoring, your team can outsource accounts receivable management and keep the focus on B2B services while the pros handle the debt recovery side of things.

What are the Benefits of Accounts Receivable Factoring?

The perks of accounts receivable factoring are huge when the economy gets bumpy. Instead of staring at factored accounts receivable and hoping for a check, you get paid by the factor instantly. This receivable factoring model changes the game by letting you:

- Stop chasing checks: Professional B2B debt collection is now the factor’s job.

- Get instant liquidity: No more waiting 30 or 60 days to see your money.

- Protect your cash flow: Keep enough in the bank for daily operations.

- Invest in growth: Use that cash to grab new opportunities immediately.

- Keep vendors happy: Pay your own bills on time or even early.

It really just frees you up from the administrative nightmare of bad debt recovery so you can actually run your business.

Types of Accounts Receivable Factoring

Accounts receivable factoring falls into the following broad categories:

Recourse & Non-Recourse Factoring

Factoring accounts receivable with recourse means you’re on the hook if your customer never pays. If you want better credit risk mitigation, you go with non-recourse factoring, where the factor takes the loss, but they’ll charge you a higher fee for that safety net.

Notification & Non-Notification

In a notification setup, the factor tells your customer where to send the payment. With non-notification, the buyer never even knows you’re using a working capital financing partner.

Spot & Regular

A spot deal is just a one-off for a single invoice. Regular factoring is more like a credit line where you can draw and redraw funds as you send out new bills.

How Much Does Accounts Receivable Factoring Cost?

The following are the typical costs associated with accounts receivable factoring

- For accounts receivable finance, a factoring fee of between 1% and 5% is incurred. The actual rate, however, might be determined by a number of variables. These variables include invoice volume, the caliber of customers, the industry risk, and the particulars of the contract.

- In addition to an initial brokerage fee of up to 5%, some factoring agencies may impose a one-time setup fee to open your factoring account. This amount might range from 500 to 2,500 dollars.

- The billing procedure has an impact on the factoring fee as well. The majority of factoring financing adheres to non-progress billing. Standard invoicing and cash payments for time and materials or commodities and services are all included. Progress billing, which often has a higher factoring cost, is used for ongoing invoices that are paid in installments, like a construction project.

- Deciding between recourse and non-recourse business factoring is another factor. Because the factor takes on greater risk than recourse factoring, it also has tougher standards.

Which Companies Use Accounts Receivable Factoring?

You’ll see this all over the B2B services world, but it’s a staple for:

- Logistics and Trucking: Where fuel needs to be paid for long before the client pays the bill.

- Staffing Agencies: Because payroll happens every week, but clients might take a month to pay.

- Construction Trades: Where everyone is waiting for the person above them in the chain to settle up.

Conclusion:

Tapping into accounts receivable factoring is a smart move if you need a quick boost in liquidity management. That said, pairing this with a solid debt recovery agency in India to keep your accounts receivable management tight is the best way to save money and stay profitable in the long run.

FAQs

1. Is accounts receivable factoring the same as a bank loan?

Not really. While both help with working capital financing, a bank loan creates debt on your balance sheet that you have to pay back monthly. With accounts receivable factoring, you’re essentially selling an asset for cash today. It’s much faster to get approved for and doesn’t require the same collateral as a traditional loan.

2. Will my customers know I’m using factoring of receivables?

It depends on the setup you choose. In a notification deal, the debt recovery agency in India will let your client know where to send the payment. However, many businesses prefer “non-notification” AR factoring, where the process is invisible to the customer, so you keep your internal billing looking the same.

3. What happens if a customer refuses to pay an invoice?

This comes down to whether you choose factoring accounts receivable with recourse or non-recourse. If it’s a recourse deal, you’ll have to buy the invoice back or swap it for a fresh one. If you opted for non-recourse, the factor takes the hit, which is the ultimate form of credit risk mitigation.

4. Can I choose which invoices I want to factor?

Yes. With “spot” receivable factoring, you can pick a single large invoice to bridge a gap. If you have constant needs, you might go for a regular agreement where you factor everything to keep your cash flow optimization steady month after month.

5. How long does it take to get the cash?

Once your account is set up with a working capital financing partner, you can usually get your funds within 24 to 48 hours of submitting an invoice. This speed is why so many B2B services rely on it—it’s much faster than waiting for a standard bank check to clear.

6. Does this help with bad debt recovery?

Absolutely. Since the factor specializes in B2B debt collection, they have the tools to ensure invoices get paid on time. By letting them handle the follow-ups, you’re essentially outsourcing your accounts receivable management to experts, which naturally reduces your late payments and overhead.