Most of us picture a man as a businessman, entrepreneur, or self-employed individual. However, the reality is more balanced. Women own and operate approximately 20% of Indian MSMEs. Over the past decade and a half, millions of thriving women-owned businesses have been created as a result of bank accounts and credit extensions geared toward women. Through credit or loans, businesses can grow, create more economic value, and jobs, as well as generate returns for the lender. What are the differences between how men and women access and repay loans in this context? Yes, it is.

In microfinance, small loans (that grow in size over time) are extended to women on the basis of social underwriting, one of the biggest success stories in credit extension to women. The RBI regulates microfinance loans to women in India, as it does with other types of loans. Those borrowers who are women who are enrolled in the formal credit system. In this sector, default rates have been remarkably low and growth has been strong over the past decade.

In spite of individual differences, men and women behave differently when it comes to money and finances. The following are some general trends:

1. Earning:

Most countries around the world have a significant gender pay gap, with women earning less on average than men. This is influenced by a variety of circumstances, including:

- Occupational segregation: Most women work in low-paying jobs and industries, whereas men are more likely to work in high-paying fields.

- Discrimination: Women may face discrimination in hiring, promotion, and pay, resulting in lower wages than men.

- Unpaid caregiving responsibilities: Women are more likely to take on unpaid caregiving responsibilities, which can make it difficult to work full-time or pursue higher-paying jobs.

- Negotiation skills: It has been found that women are less likely than men to negotiate their salaries, resulting in lower starting salaries and slower wage growth.

- Education and experience:

Women may have less access to education and training than men, limiting their earning potential.

2. Spending:

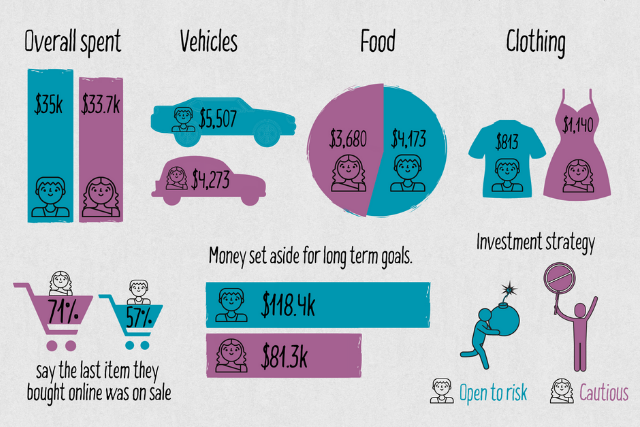

The female population tends to be more budget-conscious than the male population, preferring to save and spend carefully over making impulse purchases. The tendency of men to spend on luxury items or large purchases is the opposite of that of women.

3. Investing:

Generally, women are more cautious in their investment strategies than men are in terms of taking financial risks and investing in high-risk, high-reward opportunities such as stocks.

4. Debt:

According to the CDC, men carry more debt than women, due primarily to increased levels of student loans and credit card debt. Women are more likely to fear the impact of debt on their credit scores and future financial opportunities, while men may be more fearful of the financial burden brought by debt.

5. Financial fears

Men and women can experience financial fears, but there may be some differences in the specific fears they experience:

- Job loss: Both men and women may fear losing their jobs, but men may feel more pressure to be the primary breadwinner and experience greater anxiety.

- Retirement: Because of gender pay gaps, lower lifetime earnings, and caregiving responsibilities, women may worry that they won’t have enough money for retirement.

- Emergency expenses: Men and women may worry about unexpected emergency expenses, but women may worry more about paying medical expenses due to their higher healthcare costs and greater likelihood of taking care of children and aging parents.

- Investing: Women may be more hesitant to invest and take financial risks, which can negatively impact their long-term financial plans.

6. Financial planning:

Women tend to seek financial advice and engage in long-term financial planning, while men may rely more on their own intuition.

7. Negotiation:

Research shows that men are more likely to negotiate salary and other financial arrangements, while women are more likely to accept the initial offer.

8. Confidence:

Men may be more confident in their financial decisions even when they are not well-informed, while women may be more hesitant to take risks and make decisions without feeling fully informed.

9. Women are more conservative about spending:

Business spending by women may be more conservative than by men. Women business owners tend to have lower levels of debt and lower average expenses than their male counterparts, according to studies. When it comes to running a business, women may also prioritize cost-effectiveness and practicality over extravagant spending.

10. Women are better at self-monitoring their money:

It may be more likely for women to seek financial advice and engage in long-term financial planning, which could contribute to a greater sense of control and self-monitoring. Additionally, societal expectations and cultural norms may emphasize women’s responsibility for managing household finances, which could affect women’s self-monitoring of money.

11. Women have lesser default rates than men:

According to studies, women default on loans at a lower rate than men. A number of factors could contribute to this, including:

- Taking on fewer loans or loans with lower risk profiles may be more common among women than among men.

- There is a lower likelihood of women defaulting on their loans due to their lower debt-to-income ratios.

- Financial advice and guidance may be sought by women more often before taking on a loan, resulting in more informed and responsible borrowing decisions.

- As a result, women may have more stable employment and income compared to men, which reduces their risk of defaulting on their loans.

12. Compared to men, women get slightly better returns on their investments:

The following factors may contribute to this trend:

- Risk aversion: Women tend to prefer more conservative investments that offer lower potential returns but also lower risks when it comes to investing.

- Patience: Women often hold onto their investments for a longer period of time and avoid impulsive buying and selling that can negatively affect returns.

- Diversification: Women may be more likely to diversify their investments across a variety of asset classes and sectors, which can help to minimize risk and optimize returns.

- Lower trading costs: Women tend to trade less frequently and have lower trading costs than men, which can lead to higher overall returns.

These are general trends, and attitudes and behaviors toward money and finances may vary greatly among individuals. Approach each person and each relationship with an open mind and a willingness to understand their unique viewpoint.

FAQs

1. What is the credit score of a woman compared to that of a man?

Ans: The average credit score of the two genders is now identical. Men and women carry essentially the same level of credit card debt.

2. Do women perform better in finance than men?

According to several studies, women often earn higher returns from investing than men do. According to a recent academic study, ladies outperform men by up to 1% a year when it comes to investing.

3. Can a husband and wife have different credit scores?

There is no such thing as marriage credit scores. Credit histories and scores do not merge when you get married. Credit accounts used by your spouse cannot affect you

")